Insurance discounts for drivers can slash your premiums by hundreds of dollars annually. Most people leave money on the table by not knowing what discounts they qualify for.

At DriverEducators.com, we’ve compiled the legitimate ways to reduce your insurance costs without cutting corners on coverage. This guide walks you through the discounts available, how to qualify for them, and strategies to maximize your savings.

What Discounts Actually Lower Your Premium

Safe Driving Records Pay Off

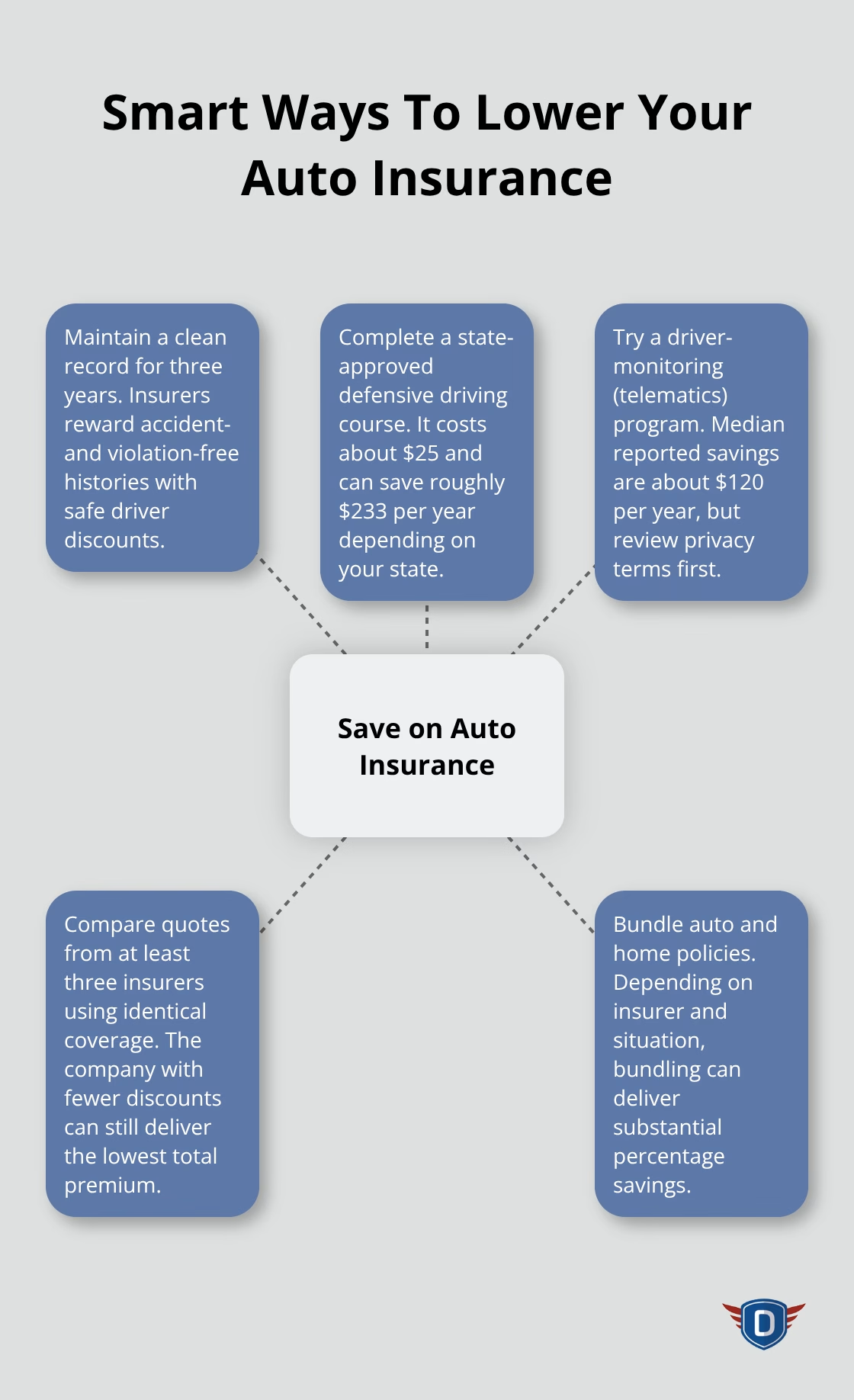

A clean driving record qualifies you for discounts that can save hundreds annually. Safe driver discounts typically apply when you avoid accidents and moving violations for three years, though some insurers extend this window. According to Consumer Reports, driver-monitoring programs save a median of about $120 per year, though you should verify what data is used and how it affects your privacy.

Student and Safety Feature Discounts

Good grades matter if you’re a student. Many insurers offer discounts for students maintaining a B average or higher, particularly those living away from home, though eligibility varies by insurer and state. Safety features on your vehicle directly impact premiums. Vehicles equipped with automatic emergency braking, blind-spot monitoring, and strong crash-test ratings reduce your risk profile and may lower your costs.

Vehicle Selection and Policy Structure

Vehicle choice matters more than most drivers realize. Before purchasing a car, compare prospective insurance costs across different models-premiums depend on the vehicle’s price, repair costs, safety record, and theft risk. Bundling auto with homeowners insurance can save up to 25% on premiums according to major insurers, though results vary by provider. Paying your annual premium upfront instead of monthly can lower your total cost, especially for longer-term terms, since monthly installments carry processing fees.

Deductibles and Mileage Adjustments

Increasing your deductible from $500 to $1,000 cuts annual premiums by about 20–25%, saving roughly $464–$525 per year (as long as you can cover the higher out-of-pocket cost if needed). If you drive fewer than 10,000 miles yearly, low-mileage discounts can save about $116 annually. The real strategy isn’t chasing every discount-it’s comparing rates across at least three insurers using identical coverages, limits, and deductibles to ensure you’re making a true apples-to-apples comparison.

What Actually Matters Most

Many drivers overlook that the final premium matters more than the number of discounts available. The insurer with fewer advertised discounts can still offer the lowest total price. Your next step involves identifying which discounts apply to your specific situation and then testing them against competing quotes.

How to Qualify for These Discounts

Complete a State-Approved Defensive Driving Course

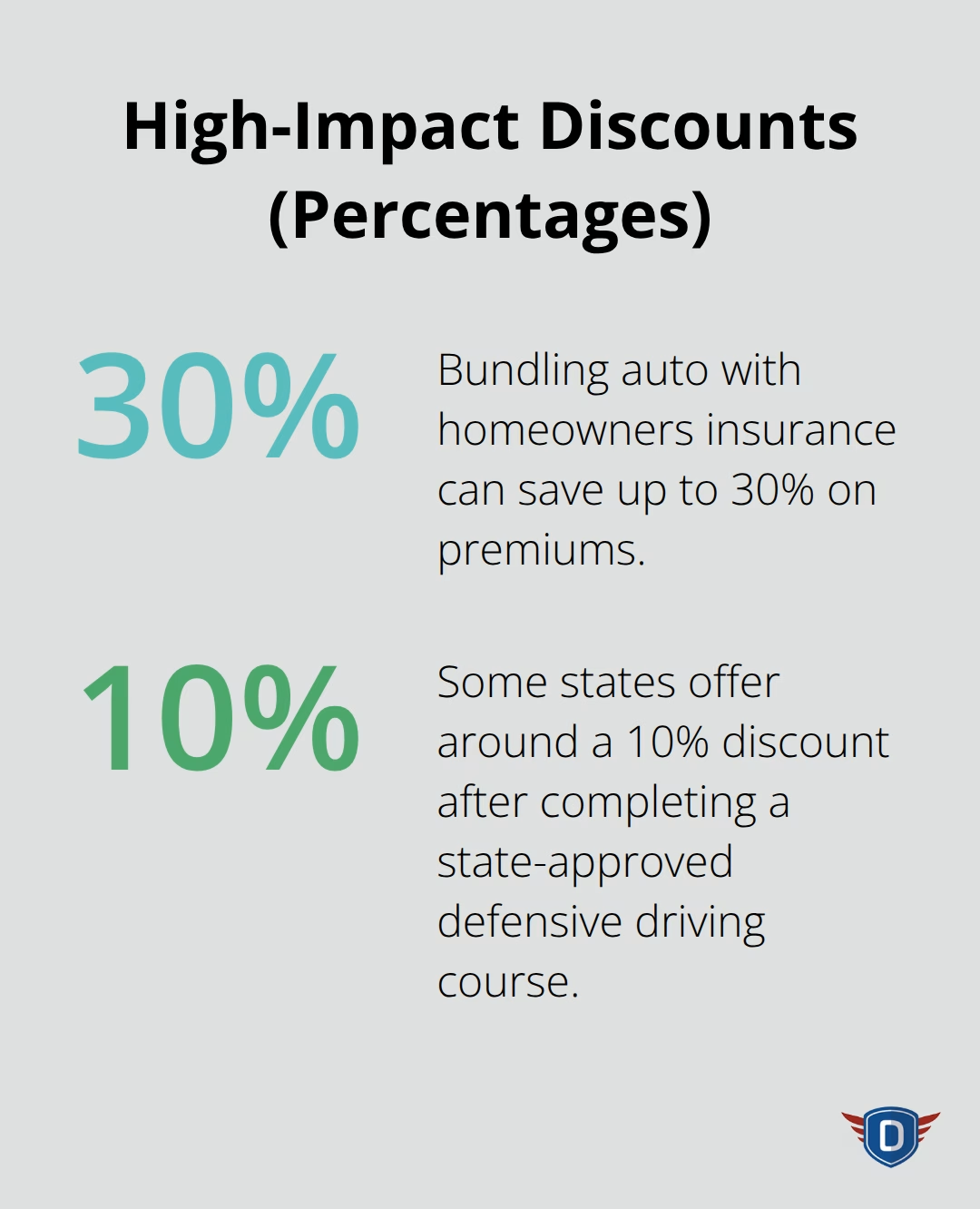

State-approved defensive driving courses deliver measurable savings when you finish through an accredited provider. These programs teach crash avoidance strategies, safe following distances, and decision-making techniques that insurers recognize and reward. A state-approved course costs around $25 and takes roughly five hours to complete, yet it saves about $233 per year according to Consumer Reports. Some states offer around 10% discounts after finishing the course, making the return on investment immediate. You must finish before your next renewal date and request the discount when you quote or renew your policy. Many drivers complete the course but fail to inform their insurer, leaving the savings unclaimed.

Build and Maintain a Clean Driving Record

Your driving record matters more than most other factors combined. You qualify for safe driver discounts when you maintain an accident-free and violation-free history for three years. Consumer Reports data shows that drivers who avoid claims see meaningful reductions at renewal. If violations or accidents already appear on your record, focus on building a clean three-year window moving forward. Some states allow expunging older points or removing them after completing a defensive driving course, so check your state’s DMV rules for specific eligibility.

Bundle Your Auto and Home Policies

Bundling auto with homeowners insurance delivers substantial savings without requiring a clean record. You can save up to 30% on premiums, though results vary by insurer and your specific situation. The savings apply whether you have a perfect record or not, making bundling an immediate action step regardless of your driving history.

Shop Multiple Insurers for the Best Rate

Comparing quotes across different insurers reveals which company offers the lowest total premium for your specific profile. You must use identical coverages, limits, and deductibles when requesting quotes to ensure an accurate apples-to-apples comparison. The insurer with fewer advertised discounts can still offer the lowest final price, so focus on the total cost rather than the number of discounts available. Testing your profile against at least three competitors takes roughly 15–20 minutes online and often uncovers savings of $300–$500 annually.

Take Action Before Your Next Renewal

Your next step involves identifying which discounts apply to your situation and then testing them against competing quotes. Contact your current insurer to confirm which discounts you already qualify for, then request quotes from competitors using the same coverage details. This comparison reveals whether staying with your current insurer or switching makes financial sense. Once you’ve selected the best option, you’re ready to explore additional strategies that maximize your overall savings.

How to Actually Save Money on Your Next Policy

Compare Quotes Using Identical Coverage

Comparing quotes from three different insurers takes about 15–20 minutes online but often reveals $300–$500 in annual savings. The critical step most drivers skip is requesting quotes using identical coverage limits and deductibles across all three companies. If you change deductibles between quotes, you’re not comparing apples to apples-you’re just confusing yourself. Start with your current policy details: note your liability limits, collision deductible, comprehensive deductible, and any optional coverages like uninsured motorist protection. Then request quotes from at least two competitors using those exact same specifications.

Many drivers assume their current insurer offers the best rate, but Consumer Reports data shows that 30% of drivers switched insurers in the past five years and saved a median of about $461 annually. That’s real money. The insurer with fewer advertised discounts often undercuts competitors with dozens of discount offers, so focus entirely on the final total premium rather than counting how many discounts you qualify for.

Review Your Coverage Annually

Annual coverage reviews catch outdated protection that wastes your money. Your situation changes-your car ages, your driving patterns shift, your financial circumstances evolve-yet most drivers renew the same policy year after year without questioning whether it still fits. If your vehicle is now worth $5,000 or less according to Kelley Blue Book or Edmunds, carrying collision and comprehensive coverage becomes financially illogical; dropping these optional coverages can save around $1,165 per year depending on your current deductibles.

Older drivers often see premiums decrease with age, but rates can rise after age 70, so shopping annually becomes even more important in your later years. Life changes-moving to a new location, changing jobs, adding household members-create natural moments to re-evaluate your coverage and identify potential savings.

Uncover Lesser-Known Discounts

Lesser-known discounts hide in plain sight: group policies through your employer or professional associations often beat individual rates, long-time customer loyalty discounts reward staying with one insurer for years, and some companies offer dividends of 5–20% through mutual insurer arrangements like Amica and NJM. Ask your insurer directly which discounts you currently don’t qualify for, then work backward-if you’re missing a low-mileage discount, track your actual annual miles; if you’re missing a good-student discount, verify the grade requirement; if you’re missing a safety-feature discount, confirm which vehicle technologies your insurer recognizes. Bundling your auto policy with homeowners or renters insurance cuts your total premiums by up to 30%, rewarding customer loyalty across multiple policies.

Take Action Before Renewal

Contact your insurer before renewal to claim discounts you’ve overlooked, then test competing quotes to ensure you’re actually getting the lowest rate available. Request quotes from at least three insurers using your current coverage specifications. This comparison reveals whether staying with your current insurer or switching makes financial sense. Once you’ve identified the best option, you’ve positioned yourself to lock in real savings on your next policy.

Final Thoughts

Insurance discounts for drivers represent real money in your pocket, but only if you claim them. Contact your current insurer and confirm which discounts you already qualify for but haven’t claimed. Then request quotes from at least three competitors using identical coverage details to see if switching saves money.

Drivers who complete defensive driving courses and maintain clean records develop safer habits that reduce accident risk. At DriverEducators.com, our traffic school programs teach crash avoidance strategies and safe driving techniques that qualify you for insurance discounts while making you a safer driver. Our Basic Driver Improvement course takes four hours and helps you avoid points and insurance increases after a moving violation.

Lower premiums compound over years-saving $300 annually means $3,000 over a decade. Start today by identifying which discounts apply to your situation, then test competing quotes before your next renewal date.