Your insurance premium doesn’t have to stay the same year after year. An insurance discount for drivers is often just a few simple steps away, whether you have a clean driving record, good grades, or multiple policies bundled together.

At DriverEducators.com, we’ve seen firsthand how drivers leave hundreds of dollars on the table by not knowing what discounts they qualify for. This guide walks you through the discounts available, how traffic school courses can lower your costs, and the practical steps to maximize your savings.

Which Insurance Discounts Actually Pay Off

Safe Driver Discounts Reward Clean Driving Records

Safe driver discounts rank among the most common auto insurance discounts available, and maintaining a clean record over time maximizes your savings. A single accident or traffic violation wipes out years of safe driving benefits, so this discount demands consistency. The financial impact is substantial-drivers with clean records save significantly compared to those with violations, making this the easiest discount to understand and the hardest to lose once you have it.

Good Student Discounts Target Academic Performance

Good student discounts apply directly to your GPA, typically requiring around a 3.0 or higher (though thresholds vary by insurer). This discount recognizes that academic responsibility often correlates with driving responsibility. If you’re a teen or young adult still in school, this discount can reduce your premium by a meaningful amount, especially important since adding a teen driver typically increases premiums by roughly $1,000–$2,000 per year according to Consumer Reports. You’ll need to provide proof of your grades when applying or at renewal to claim the discount. Not every insurer offers this discount with identical requirements, so asking directly about eligibility during the quote process matters. College students living away from home may also qualify for distant student discounts if your vehicle stays parked at your parents’ address, with distance requirements varying by carrier.

Bundling Policies Creates the Largest Savings

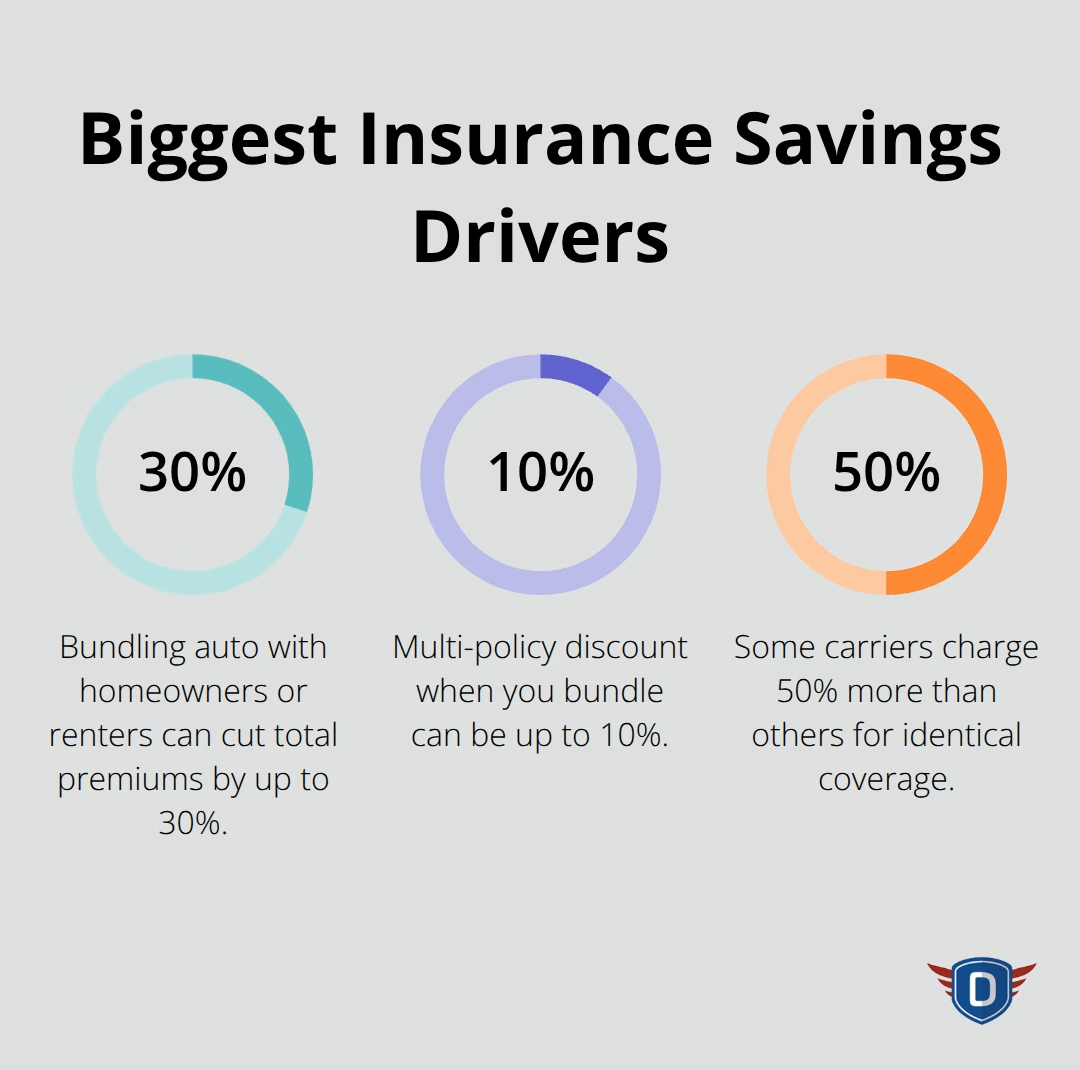

Bundling auto insurance with homeowners or renters insurance is the single most effective way to lower your premium. Consumer Reports research shows that bundling can cut your total premiums by up to 30%, though results vary by insurer and location. This discount works because insurers reward customer loyalty and reduce their administrative costs when managing multiple policies under one account. The savings from bundling often exceed what you’d gain from combining several smaller discounts individually. When you’re comparing quotes, always request bundled rates alongside standalone auto quotes to see the real difference. Some insurers like Farmers and Geico list many discounts, but bundling typically delivers the largest single reduction in your annual cost.

These three discount categories form the foundation of most drivers’ savings strategies, but they represent only part of the picture. Defensive driving training opens additional pathways to lower your costs while simultaneously improving your actual driving skills.

How Traffic School Cuts Your Insurance Costs

Defensive Driving Courses Deliver Measurable Savings

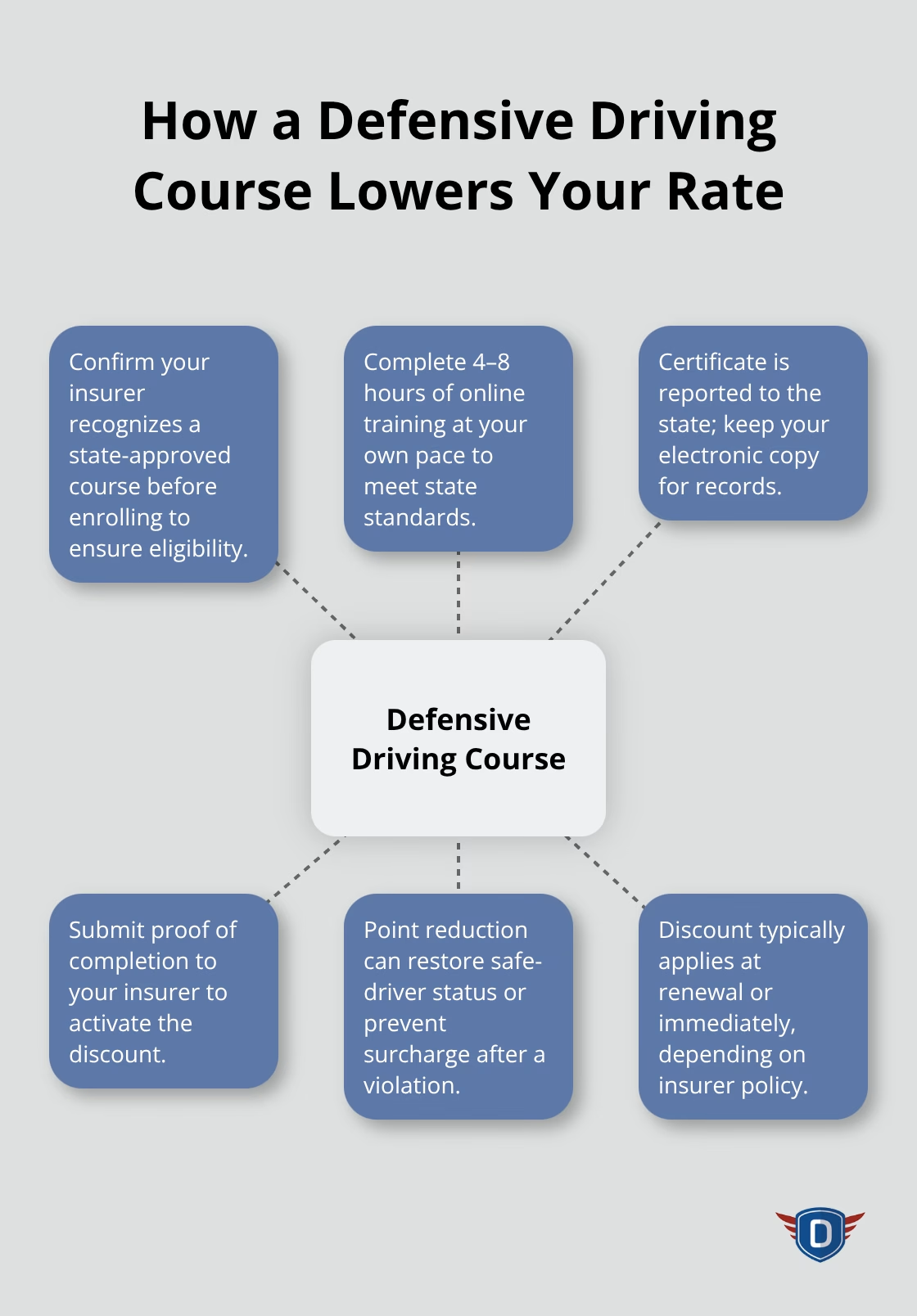

Defensive driving courses offer the most direct path to an insurance discount after a traffic violation. Your insurer must recognize the course your state approves, so calling them before you enroll matters. Florida-approved traffic school programs follow strict guidelines set by the Florida Department of Highway Safety and Motor Vehicles, which means they meet the standards insurers expect. These courses run four to eight hours depending on the program level, and you complete them entirely online at your own pace. Once you finish and receive your certificate, it gets reported directly to the state, and you submit proof to your insurer to claim your discount. The financial investment in a few hours of coursework pays for itself quickly through the discount you receive.

Point Reduction Programs Improve Your Driving Record

Point reduction programs operate differently than simple discounts. When you complete a state-approved course, the Florida Department of Highway Safety and Motor Vehicles can reduce points on your driving record, which directly improves your standing with insurance companies. A single moving violation typically adds points that stay on your record for three to five years, and each point signals risk to insurers, pushing your premium higher. Removing even one or two points through a defensive driving course can prevent your insurer from raising your rate after a violation, or it can help you qualify for discounts you’d otherwise lose.

How Insurers Apply Point Reductions to Your Policy

The timing of point reduction matters significantly. Some insurers reset your safe driver discount eligibility after you complete a qualifying course, while others simply stop penalizing you for the violation. Your insurer’s specific rules vary, which is why asking them directly about how point reduction affects your particular policy saves you from guessing. State-approved courses ensure the points reduction applies correctly and your insurer recognizes the completion immediately.

Getting Your Certificate Recognized by Your Insurer

After you finish your course, you receive an electronic certificate that gets reported directly to the state. You then submit proof of completion to your insurer to claim your discount. This process typically takes just a few days, and most insurers apply the discount at your next renewal or immediately, depending on their policy. Having your certificate in hand before contacting your insurer speeds up the process and eliminates back-and-forth communication about whether your course qualifies.

With your driving record improved and your insurance discount secured, the next step involves taking control of your entire premium through strategic comparison and negotiation.

How to Lock in the Lowest Insurance Rate

Compare Quotes from Multiple Insurers

Comparing quotes from multiple insurers is non-negotiable if you want the best price. Consumer Reports data shows that about 30% of policyholders switched insurers in the past five years, and those who switched saved a median of $461 per year simply by shopping around.

Yet most drivers never request more than one quote. When you do compare, request identical coverage limits and deductibles across all quotes so you’re genuinely comparing apples to apples.

The difference between insurers for the same driver and vehicle can be dramatic-some carriers charge 50% more than others for identical coverage. Getting quotes from at least three different insurers takes about 15 minutes online and directly translates to hundreds of dollars in annual savings. Many major providers like Progressive, Nationwide, Liberty Mutual, and Allstate allow you to customize your coverage limits and deductibles right on their websites so you can see exactly how each choice affects your rate.

Ask About Every Discount You Qualify For

Most drivers fail to mention every discount they qualify for when requesting a quote, which means they miss savings they’re entitled to claim. When you request a quote, explicitly ask the agent or representative to list all available discounts for your specific situation-safe driver, bundling, low mileage, automatic payment, paperless billing, good student, military, and any employer-based programs.

Some insurers like Farmers and Geico advertise numerous discounts but don’t automatically apply them unless you ask. Bundling auto with homeowners or renters insurance offers a multi-policy discount of up to 10%, so always request a bundled quote alongside your standalone auto rate to see the real difference.

Time Your Policy Review Strategically

The timing of your policy renewal matters significantly. Annual reviews let you identify new discounts you’ve become eligible for since your last policy started-you might have improved your credit score, reduced your annual mileage, or completed a defensive driving course that now qualifies for a reduction.

Waiting until renewal day to shop means you’re acting reactively instead of proactively, and you may miss the opportunity to switch carriers before your current premium increases take effect. Insurers often hold renewal quotes for 30 to 60 days, so start shopping 60 days before your policy ends to give yourself time to switch if a competitor offers better rates.

Final Thoughts

The path to lower insurance premiums starts with understanding what discounts you actually qualify for and taking action to claim them. Safe driver discounts, good student discounts, and bundling policies form the foundation of most savings strategies, but the real money comes from comparing quotes across multiple insurers and asking about every discount available. Drivers who switch insurers save a median of $461 per year, while those who complete defensive driving courses save around $233 annually-these are actual savings that appear on your bill when you follow through.

Your next move requires three concrete steps. Start by requesting quotes from at least three different insurers with identical coverage limits and deductibles, then explicitly ask about every discount you qualify for including safe driver, bundling, low mileage, automatic payment, and paperless billing. If you’ve received a traffic violation, complete a state-approved defensive driving course to reduce points on your record and qualify for additional savings that lower your insurance discount for drivers even further.

Schedule an annual policy review 60 days before your renewal date so you can switch carriers if a competitor offers better rates before your premium increases take effect. Taking control of your insurance costs isn’t complicated-it just requires you to shop strategically, ask the right questions, and complete a defensive driving course through DriverEducators.com when you need to reduce points on your record.