The moments after a car accident are a blur of adrenaline and confusion. It’s a stressful situation, but knowing exactly what to do can protect you, both legally and financially. Right after a crash in Florida, you need to think clearly: secure the scene, check for injuries, call 911 if necessary, and swap essential information with the other driver—all while being very careful about what you say. A solid understanding of the law is your best defense, and becoming a more skilled driver is your best offense.

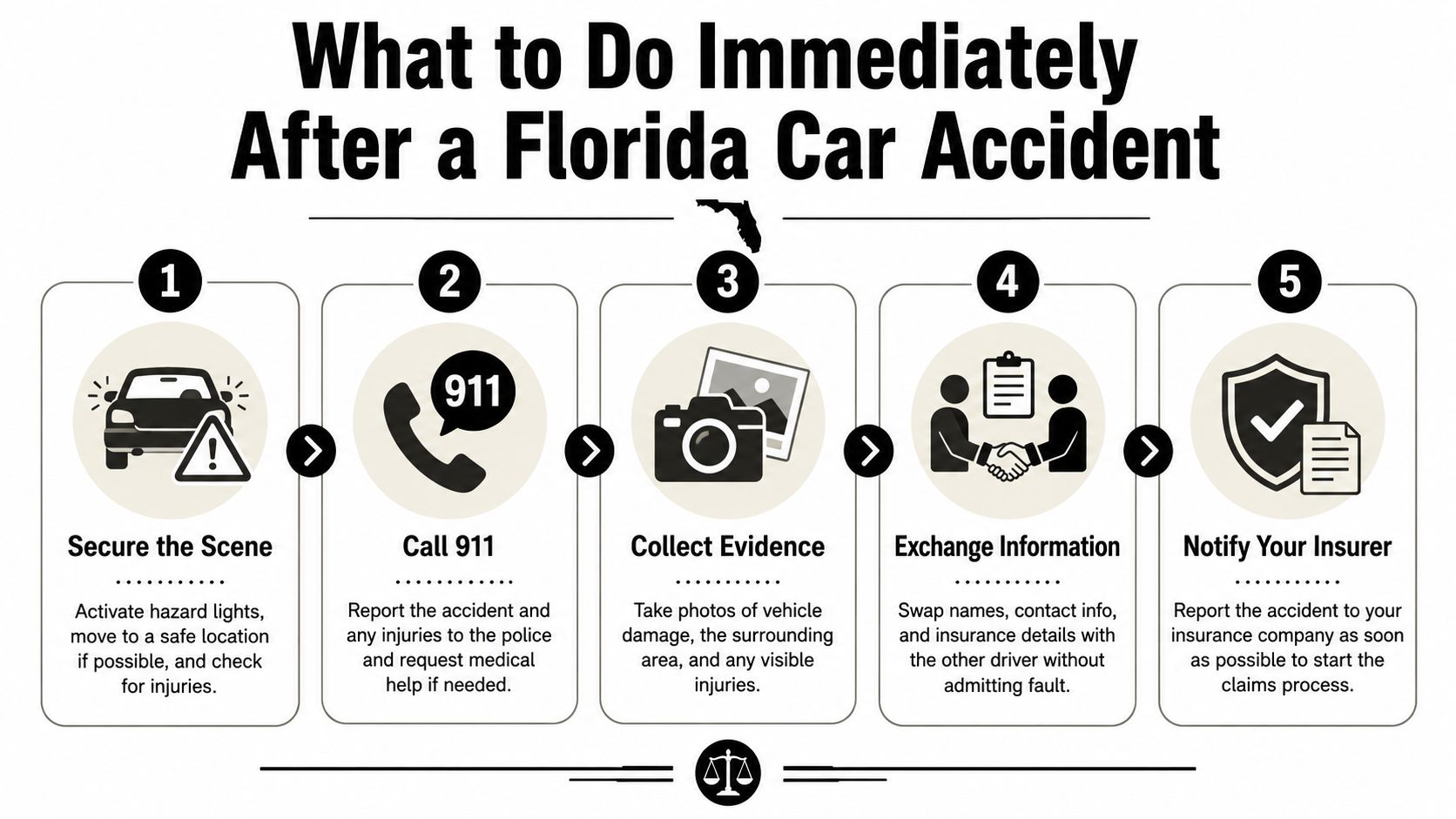

What to Do Immediately After a Florida Car Accident

An accident is a high-stress test, and clear thinking is your best asset. The steps you take in those first few minutes and hours are absolutely critical for your safety and any future insurance claims. Becoming a truly prepared driver starts with mastering these initial actions.

First things first: safety. If you can, move your car out of the flow of traffic to prevent another collision. Immediately flip on your hazard lights to warn oncoming drivers.

Secure the Scene and Check for Injuries

Once you’re in a safer spot, check on yourself and your passengers. Adrenaline is a powerful pain-masker, so you might not realize you’re hurt right away. If anyone seems injured, no matter how minor it appears, you need to make that a priority when you call for help.

Speaking of calling for help, Florida law requires you to report any accident that involves:

- An injury or a death

- A hit-and-run

- A driver who seems intoxicated

- Property damage that looks like it’s $500 or more

Honestly, with the cost of car repairs today, almost any fender-bender will easily pass that $500 mark. When in doubt, call 911. A police report creates an official, unbiased record of the incident, which is incredibly valuable for your insurance claim.

Gather Evidence and Exchange Information

While you’re waiting for the police to arrive, start documenting everything. Use your phone to take photos of both cars from every angle. Get pictures of the wider scene, including any skid marks, debris on the road, and nearby traffic signs. This visual proof can be a game-changer.

Next, you are required to exchange information with the other driver. Make sure you get their:

- Full name and contact info

- Insurance company name and policy number

- Driver’s license number

- License plate number

It’s vital to be polite and cooperative, but never say things like “I’m so sorry” or “This was my fault.” Statements like that can be seen as an admission of guilt and used against you down the road.

Getting a handle on what to do right away is key, and some local resources offer excellent Deerfield Beach car accident guidance. For a complete playbook on handling the entire process, check out our comprehensive guide on what to do after a car accident. Mastering these steps is a fundamental part of being a prepared, responsible driver, and our courses are designed to reinforce this crucial knowledge.

Understanding Florida’s No-Fault Law and PIP Insurance

Florida’s approach to car accidents often throws people for a loop. We’re a “No-Fault” state, which doesn’t mean no one is ever at fault. A better way to think of it is as a “your-insurance-pays-first” system, designed to get your immediate medical bills paid quickly without waiting to determine who caused the collision.

The whole system rests on Personal Injury Protection (PIP) insurance. It’s not optional; it’s mandatory coverage for every single driver in Florida. The idea is that after a crash, you turn to your own insurance policy first to cover your injuries. Every driver must carry at least $10,000 in PIP coverage.

What Your PIP Benefits Actually Cover

Your PIP policy is the first safety net for your injuries. It’s designed to cover a big chunk of your initial medical bills and even a portion of your lost wages if you can’t work after the accident.

But here’s the catch, and it’s a big one that every Florida driver needs to burn into their memory: you have to move fast.

To get any money from your PIP benefits, you absolutely must seek medical treatment within 14 days of the accident. If you wait any longer, you could lose your right to this crucial coverage completely.

This isn’t just a suggestion—it’s a hard deadline. Missing that two-week window can leave you on the hook for thousands in medical bills you thought your insurance was supposed to handle.

The infographic below shows you the exact steps to take right after a crash to protect your health and your finances.

Following these steps is the best way to make sure you’ve documented everything you need to start your PIP claim without a hitch.

Getting the Most from Your Coverage

To really make the No-Fault system work for you, you need to know what’s in your own policy. Seriously, take a few minutes to understand your auto insurance coverage before you’re in a stressful situation. It’s the single best thing you can do to prepare.

Here’s a quick breakdown of what your PIP policy will pay for:

- Medical Bills: It covers 80% of necessary and reasonable medical expenses from the crash.

- Lost Wages: It covers 60% of any income you lose because your injuries keep you from working.

- Death Benefits: PIP also includes a $5,000 benefit in the event of a death.

Just as important is knowing what PIP doesn’t cover. It won’t pay for damage to your car, the other person’s car, or their property. To get a clearer picture of how it all fits together, you can learn more about what a no-fault accident really means. Knowing these rules isn’t just good advice; it’s a fundamental part of being a responsible driver on Florida’s roads—a skill our driver improvement courses help you perfect.

When Fault Determines Your Financial Recovery

While your PIP insurance is a great first line of defense for your initial medical bills, it has a strict $10,000 limit and won’t cover everything. So, what happens when injuries are severe and the costs skyrocket well past that cap? This is where the idea of “fault” becomes the most important factor in your financial recovery.

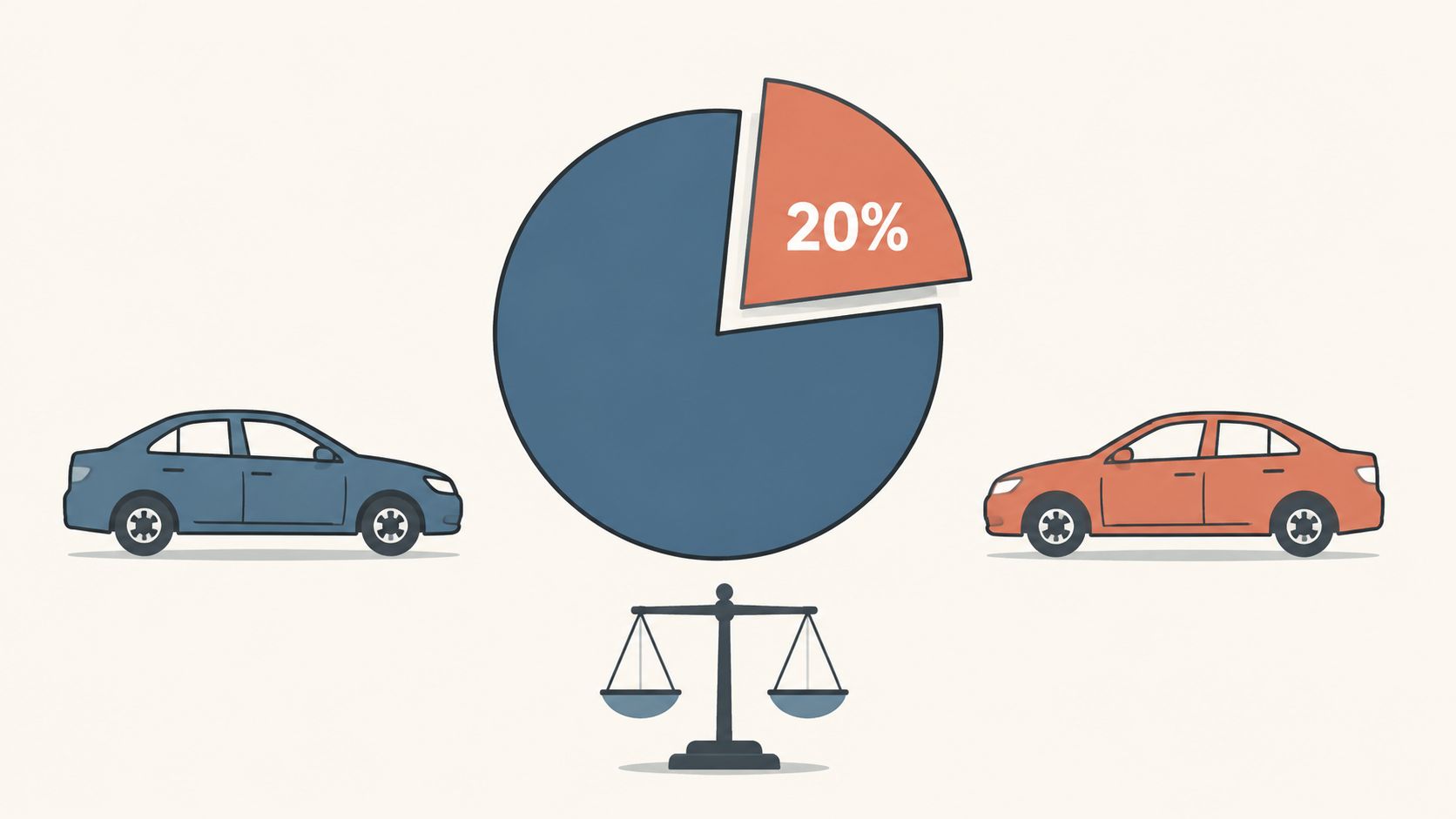

If you need to pursue compensation beyond what your PIP policy pays, you’ll run straight into Florida’s comparative negligence rule. It’s a legal concept that sounds complicated, but it’s really just a system for dividing up the financial responsibility based on each driver’s share of the blame for the crash.

How Comparative Negligence Works

Think of the total damages from an accident—every medical bill, lost paycheck, car repair, and even pain and suffering—as one lump sum. Under comparative negligence, a court or insurance company figures out what percentage of the accident was your fault. Your final compensation is then reduced by that exact percentage.

For instance, let’s say you’re awarded $100,000 for your damages, but you’re also found to be 20% at fault for causing the collision. That 20% gets shaved right off the top, meaning you’d walk away with $80,000 instead of the full amount.

The main takeaway here is powerful: even being assigned a tiny sliver of fault can have a huge financial impact, potentially costing you tens of thousands of dollars.

Why Defensive Driving Is Your Best Financial Defense

Because Florida uses this comparative negligence system, every move you make behind the wheel matters. A driver’s compensation is directly tied to their percentage of fault, which is why a deep understanding of right-of-way rules and defensive driving is so critical. You can learn more about how fault is typically assigned by reviewing Florida car accident statistics and legal interpretations.

This rule turns defensive driving from a simple safety habit into an essential financial strategy. Every decision could be analyzed to assign blame, which is exactly why our Basic Driver Improvement (BDI) and Intermediate Driver Improvement (IDI) courses are so important. We don’t just teach the rules; we instill the advanced defensive skills you need to anticipate and avoid hazards created by other drivers. Sign up today and learn how to protect yourself on the road.

Ultimately, mastering these techniques is the best way to protect yourself and minimize your liability, shielding your finances from the costly consequences of being found even partially at fault.

Understanding Accident Reporting Laws and Deadlines

After a crash, your first thoughts are probably about your car and your health. But what you do next is dictated by specific Florida laws, and not knowing them can have serious consequences. Forgetting to follow these rules isn’t a minor slip-up; it can lead to fines, a suspended license, and even sink your chances of getting paid for your damages.

First things first: when do you have to call the police? In Florida, the law is clear. You must report any crash immediately if someone is injured or killed, or if there’s property damage that looks like it will cost $500 or more to fix. With the sky-high cost of parts and labor today, even a minor fender-bender can easily top that amount. Getting a police report is non-negotiable—it creates an official, neutral record that is absolutely essential for your insurance claim.

The Clock Is Ticking on Your Legal Rights

Beyond reporting the crash, there’s another critical deadline you need to be aware of: the statute of limitations. Think of it as a countdown clock that starts the second the accident occurs. It puts a strict time limit on your right to file a lawsuit.

This isn’t a flexible guideline. If you miss this deadline, your right to seek compensation for your injuries and other losses is usually gone for good. It’s a harsh reality, but it’s designed to ensure legal matters are handled in a timely manner.

For most personal injury claims from a car accident in Florida, you now have just two years from the date of the crash to file a lawsuit. This is a recent change, making it more important than ever to act quickly.

Here’s a quick summary to help you remember the key reporting rules and legal deadlines.

Florida Accident Reporting Quick Reference

This table breaks down when you need to involve the police and how long you have to pursue legal action.

| Scenario | Police Report Required? | Key Deadline |

|---|---|---|

| Any injury or death | Yes, immediately | Two years to file a personal injury lawsuit |

| Apparent property damage of $500+ | Yes, immediately | Four years to file a property damage lawsuit |

| Hit-and-run (as a victim) | Yes, immediately | Two years for injury, four years for property |

Understanding these timelines is a huge part of being a responsible driver. Two years might sound like a long time, but it flies by when you’re dealing with doctor’s appointments and car repairs. This is the kind of real-world knowledge we emphasize in our traffic school courses, giving you the tools to protect not just your driving record, but your financial well-being too. Enroll now to ensure you’re prepared.

The Real Causes of Florida’s Most Dangerous Accidents

It’s easy to blame a sudden Florida downpour for a crash. We’ve all been there—white-knuckling the steering wheel as visibility drops to near zero. But while rain certainly makes the roads slick, the hard data tells a different, more predictable story. The biggest threat on our highways isn’t the weather; it’s the person in the other car.

Surprisingly, the vast majority of fatal accidents don’t happen in a storm. They happen on clear nights with dry roads. This is because good conditions can create a false sense of security, causing drivers to let their guard down and make deadly mistakes. The real danger is us.

So, When and Why Are These Crashes Happening?

Forget the weekday rush hour. The most dangerous times on Florida roads are weekend nights under clear skies. The highest risk for fatal accidents clusters on Fridays, Saturdays, and Sundays, with major spikes on Friday at 9 p.m. and Saturday around 11 p.m. and 2 a.m.

The numbers don’t lie. Recent statistics show that 765 deaths were caused by careless or negligent driving, and another 559 were the result of a driver failing to yield the right-of-way. These aren’t acts of God; they’re the direct result of poor decisions.

- Distracted Driving: A text message, a quick glance at the GPS, or turning around to talk to passengers—it only takes a second to cause a tragedy.

- Driver Fatigue: Driving while drowsy can be just as dangerous as driving drunk. It slows your reaction time and clouds your judgment.

- Aggressive Driving: Speeding, tailgating, and weaving through traffic are all recipes for disaster, turning a simple drive into a high-stakes gamble.

This data proves that the driver in the other car often poses a greater risk than a thunderstorm. Anticipating and reacting to their poor decisions is the core of true defensive driving.

This is exactly why a defensive mindset is so critical for Florida drivers. It’s not just about following the rules—it’s about actively spotting the warning signs and anticipating what other drivers will do before they do it. To get a better handle on this, our detailed guide explains what causes most car accidents.

Courses like our Aggressive Driver and Basic Driver Improvement (BDI) programs are built to sharpen these exact skills. We teach you how to recognize high-risk situations and give you the tools to become a safer, more prepared driver on Florida’s unpredictable roads. Don’t wait to improve your skills—register for a course today.

Turn a Traffic Ticket Into a Smarter Driving Future

Getting slapped with a traffic ticket right after an accident is the last thing anyone wants. It’s frustrating, and the potential consequences—points on your license, a damaged driving record, and soaring insurance rates—can feel overwhelming.

But here’s the thing: that ticket doesn’t have to be the final word. You have a chance to take control of the situation and turn this negative experience into a genuine positive for your driving future. Instead of just paying the fine and bracing for the fallout, you can choose a much smarter path by enrolling in a driver improvement course.

How to Turn That Ticket to Your Advantage

Think of a state-approved driver improvement course as your best tool for protecting both your license and your wallet. By choosing to take a Basic Driver Improvement (BDI) course, you’re not just dealing with one ticket; you’re making a proactive choice that pays off immediately and for years to come.

Taking a course gives you a clear edge over someone who just pays the penalty. Here’s what you stand to gain:

- Dismiss Your Ticket: When you successfully complete the course, you may be able to get the entire citation dismissed.

- Keep Points Off Your License: This is huge. You can prevent points from accumulating on your record, which helps you avoid a potential license suspension down the road.

- Stop Insurance Hikes: A ticket from an accident is a red flag for insurers. Completing a course can stop your premiums from increasing because of the violation.

Taking a course shows the court and your insurance provider that you’re responsible and serious about safe driving. It proves you’re willing to go the extra mile to sharpen your skills.

The need for skilled, defensive drivers has never been greater. In 2025, Florida had a staggering 366,300 traffic crashes—that’s an average of about 1,003 accidents every single day. These numbers underscore just how important driver education really is.

Our online BDI and Intermediate Driver Improvement (IDI) courses are designed to fit your life. They’re convenient and self-paced, giving you the knowledge you need to handle your current ticket and the defensive driving techniques to help you avoid future ones. We’ll show you how to dismiss a traffic ticket and help you get back on the road as a more confident, prepared driver. Ready to start? Find your course now.

Florida Accident Law: Your Questions Answered

After a crash, your head is spinning with questions and legal jargon can make things even more confusing. Let’s cut through the noise and get you the straight answers you need to protect yourself on Florida’s roads. Being a skilled driver means being an informed one.

What Is the Single Most Important Thing for My PIP Claim?

This one is non-negotiable: you have to see a medical professional within 14 days of the accident. That’s it. Whether you go to the ER, an urgent care clinic, or even your own family doctor doesn’t matter, but the clock is ticking.

If you miss this two-week window, your insurance company can deny your Personal Injury Protection (PIP) claim outright. You could be left holding all the medical bills, even though you paid for the coverage.

Can I Still Get Money If I Was Partially at Fault?

Yes, you can, but it’s not a simple “yes” or “no.” Florida follows what’s called a modified comparative negligence rule, which has a critical cutoff. You can collect damages as long as you are found to be 50% or less to blame for the accident.

Here’s how it works in the real world: if you’re awarded $50,000 for your injuries but a jury decides you were 20% at fault, your final payment is reduced by that 20%. You’d walk away with $40,000.

Think of it this way: every percentage point of fault the other side can pin on you comes directly out of your pocket. This is why driving defensively isn’t just about avoiding accidents—it’s about protecting your financial well-being if one happens.

How Long Do I Have to File a Car Accident Lawsuit?

The deadline, legally known as the statute of limitations, is strict and unforgiving. For any personal injuries from a car accident, you have just two years from the date of the crash to file a lawsuit. For property damage only, the window is a bit longer at four years.

If you wait too long, the door to the courthouse slams shut, and you lose your right to seek compensation forever.

Knowing these rules isn’t just for lawyers; it’s a crucial part of being a responsible Florida driver. Our courses are designed not only to teach driving techniques but also to empower you with the knowledge to protect your rights after a crash—just as important as preventing one in the first place.

At BDISchool, we believe an informed driver is a safer driver. Our state-approved online courses are designed to help you dismiss a ticket, lower your insurance costs, and truly master the defensive driving skills that matter on Florida’s busy roads. Take control of your driving record by exploring our courses at https://drivereducators.com/courses/. Don’t just deal with the aftermath of an accident—invest in your driving future and register today.