Aggressive driving consequences go far beyond traffic tickets and accident reports. Your insurance company is watching, and every reckless decision behind the wheel directly impacts what you pay for coverage.

We at DriverEducators.com know that many drivers underestimate how quickly aggressive behavior can drain their wallets. This guide breaks down exactly how insurers track your driving habits and what it costs when you don’t drive safely.

What Counts as Aggressive Driving

Road Rage and Confrontational Behavior

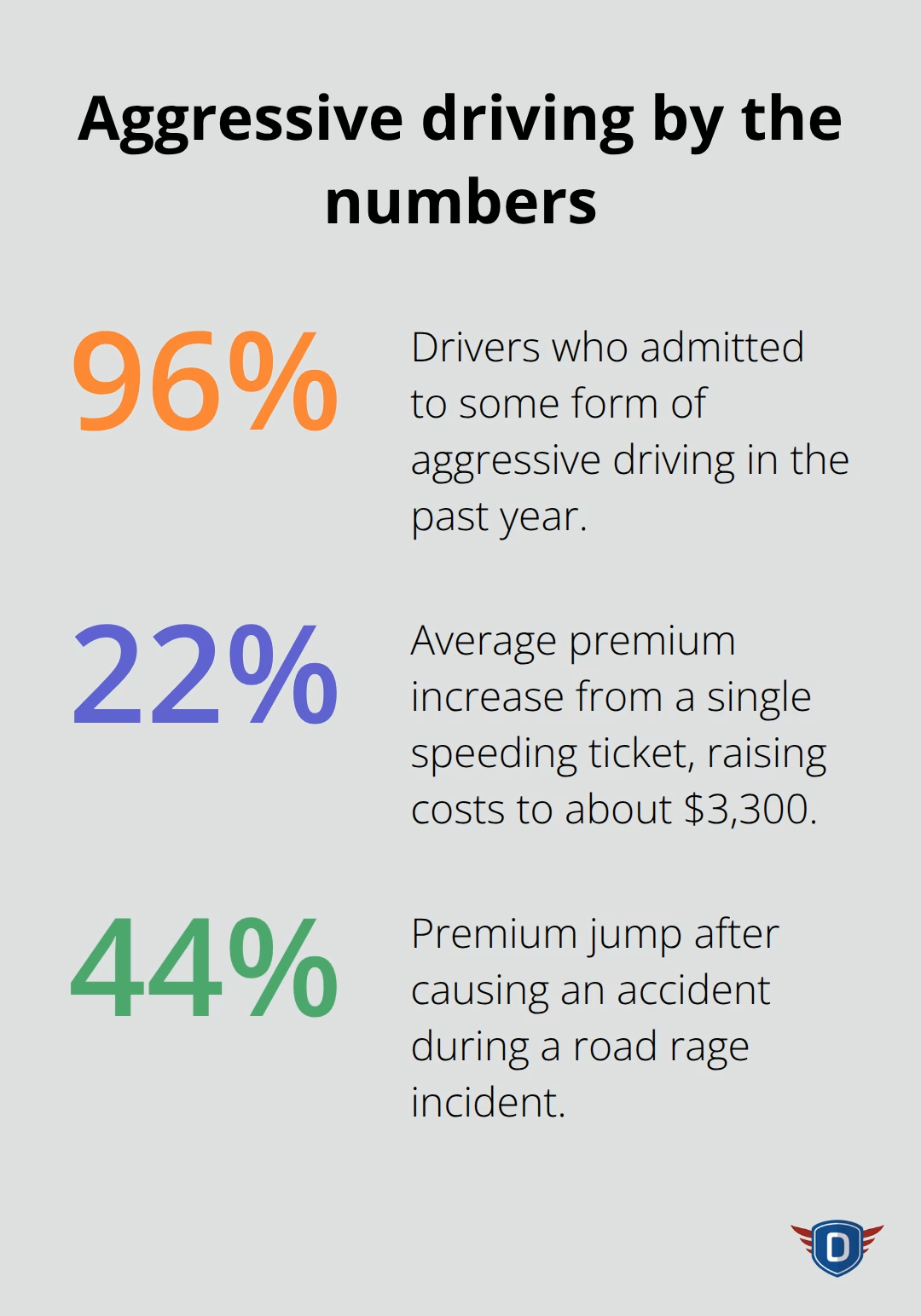

Aggressive driving isn’t just about anger behind the wheel. The AAA Foundation for Traffic Safety found that 96% of drivers admitted to engaging in some form of aggressive driving in the past year, which means most people don’t realize how often they cross the line. Road rage represents the extreme end of the spectrum, where drivers deliberately confront other motorists or make dangerous maneuvers to intimidate them. This includes brake-checking, swerving to block another vehicle, or forcing someone off the road.

Colorado has emerged as an epicenter for road rage violence per capita, and road rage deaths nearly doubled from 2018 to 2023. If you cause an accident during a road rage incident, your insurance premium can jump by about 44%, according to data from the Oklahoma Insurance Council. The financial consequences extend beyond the immediate accident-your insurer will flag you as high-risk for years.

Speeding and Reckless Maneuvers

Speeding and reckless maneuvers damage your wallet just as much as road rage. A single speeding ticket raises your annual premium from the baseline of over $2,600 to about $3,300, a 22% increase. Harsh braking and rapid acceleration signal aggressive driving patterns to insurers, and these behaviors correlate directly with more accidents and higher maintenance costs.

Insurance companies track these patterns through your driving record and, increasingly, through telematics data. When you accelerate hard or brake suddenly, you’re not just wasting fuel-you’re creating a digital footprint that insurers use to assess your risk level.

Tailgating and Unsafe Lane Changes

Tailgating and unsafe lane changes eliminate reaction time and create the conditions for costly collisions. Tailgating leaves drivers with seconds to respond to sudden stops, and in trucks with longer stopping distances, rear-end crashes become even more expensive. When you cut off other drivers or weave through traffic, you signal to insurers that you’re a high-risk driver.

The financial penalty is steep: a single accident claim averages around $70,000 when factoring in repairs, downtime, and liability. Exposure to aggressive driving increases the likelihood that other drivers will act aggressively too, amplifying overall risk on the road. If you’re confronted by an aggressive driver, the safest approach is to avoid engagement entirely-let the aggressor pass and create distance between your vehicle and theirs.

Understanding these behaviors is the first step toward recognizing how your driving habits translate into insurance costs. The next section reveals exactly how insurers monitor your actions and calculate what you owe.

How Insurance Companies Track Aggressive Driving

Your Driving Record Tells the Story

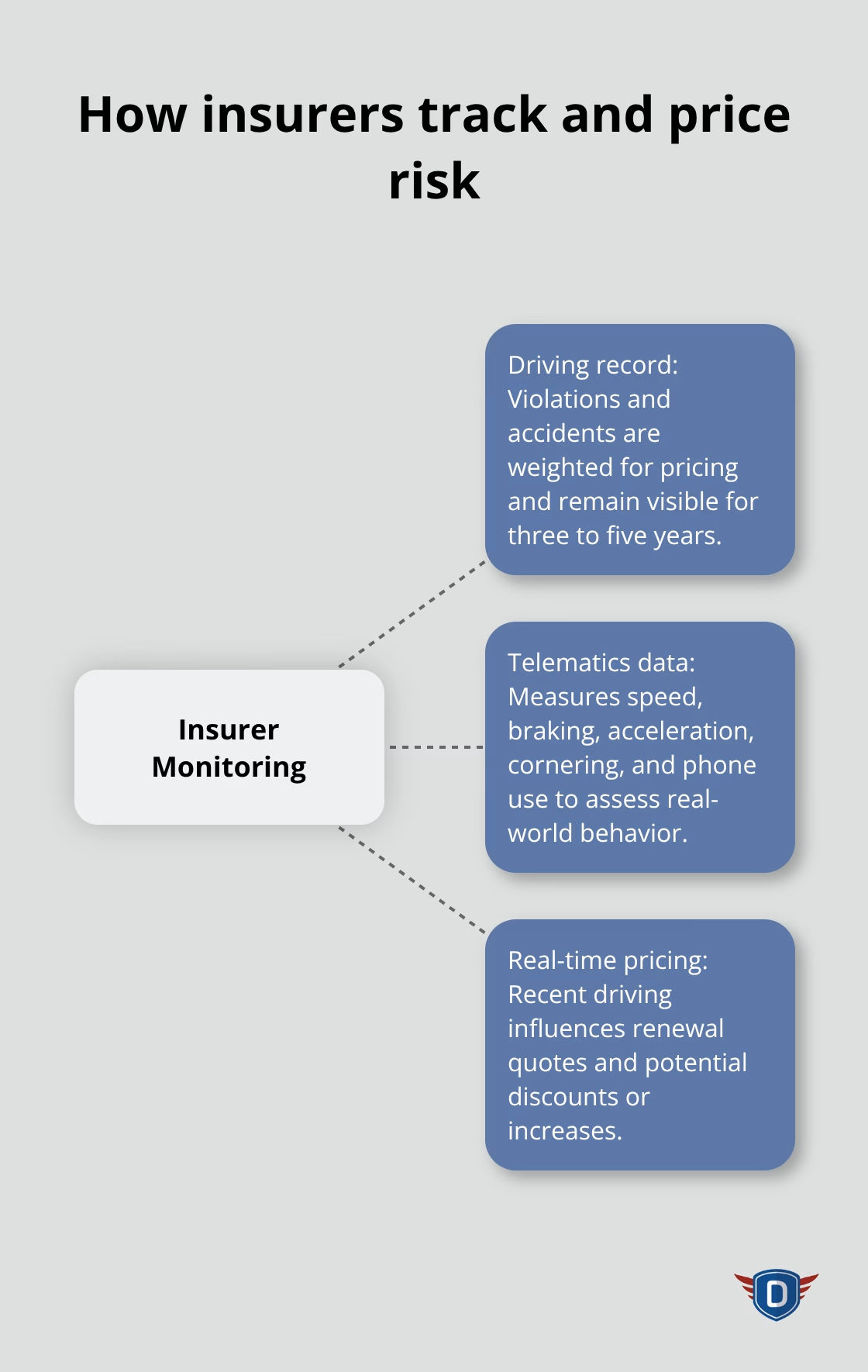

Insurance companies build a complete profile of your driving habits using three distinct methods, each one designed to catch aggressive behavior and calculate your risk. Your driving record documents every violation and accident you’ve had, and insurers weight these heavily in their pricing models. A single speeding ticket stays on your record for three to five years, depending on your state, and each violation signals to your insurer that you’re more likely to cause a claim.

When you combine multiple violations-speeding, tailgating citations, reckless driving charges-insurers classify you as high-risk, which means your premiums climb significantly and your renewal quotes become harder to negotiate. Safer driving directly reduces both the frequency and severity of claims, which means insurers reward clean records with lower rates. Conversely, drivers with a history of aggressive driving behaviors face steeper premiums because the data proves they file more claims.

Telematics Devices Capture Real-Time Behavior

Telematics devices and smartphone monitoring apps now give insurers real-time insight into your actual driving patterns, not just what shows up on your official record. These systems track speed, acceleration, braking force, cornering behavior, and even phone usage while driving, creating a digital record that’s far more detailed than any traffic citation. Insurers increasingly use this data to differentiate between drivers and price premiums more accurately based on actual behavior rather than demographics alone.

If your telematics data shows harsh braking, rapid acceleration, or speeding in school zones, your insurer can flag you as higher-risk and adjust your rate accordingly. Some insurers offer discounts for drivers who demonstrate consistent safe driving over time, while others use telematics to justify premium increases when the data reveals risky patterns.

How Real-Time Monitoring Changes Insurance Pricing

The technology shifts the insurance model from punishing past mistakes to monitoring current behavior, which means your next three months of driving can directly impact your next renewal quote. This real-time monitoring creates accountability that traditional citations cannot match-your insurer knows not just that you speed, but how often, how much, and on which roads. Telematics data allows insurers to reward safer drivers with lower premiums or discounts when behavior improves, creating a direct financial incentive for you to change your habits behind the wheel.

Understanding how insurers monitor your actions reveals why your next decision matters. The financial consequences of aggressive driving patterns show up immediately in your premium calculations.

What Your Aggressive Driving Really Costs

The Immediate Financial Penalty

A speeding ticket raises your annual premium from the baseline of over $2,600 to approximately $3,300 according to Oklahoma Insurance Council data, which means a single violation costs you $700 extra every year. If you cause an accident during aggressive driving, expect a 44% premium increase on top of that baseline, pushing your annual cost to roughly $3,744. These aren’t one-time penalties; they compound over years as violations and accidents stack up on your record. Most drivers fail to calculate the true cost because they focus only on the immediate fine, not realizing that insurance companies penalize aggressive behavior for three to five years after the violation occurs.

What a Single Accident Actually Costs

A serious collision claim averages around $70,000 when you factor in vehicle repairs, downtime, liability, and the inevitable premium spike that follows. When you add in your collision deductible of $500 to $1,000 that you’ll pay out of pocket before insurance kicks in, the total financial damage becomes staggering. The AAA Foundation for Traffic Safety confirms that safer driving directly reduces both the frequency and severity of claims, which means insurers reward clean records with substantially lower rates. Conversely, drivers with multiple violations become classified as high-risk, which means renewal quotes grow by 20 to 50% year over year.

The Five-Year Cost Comparison

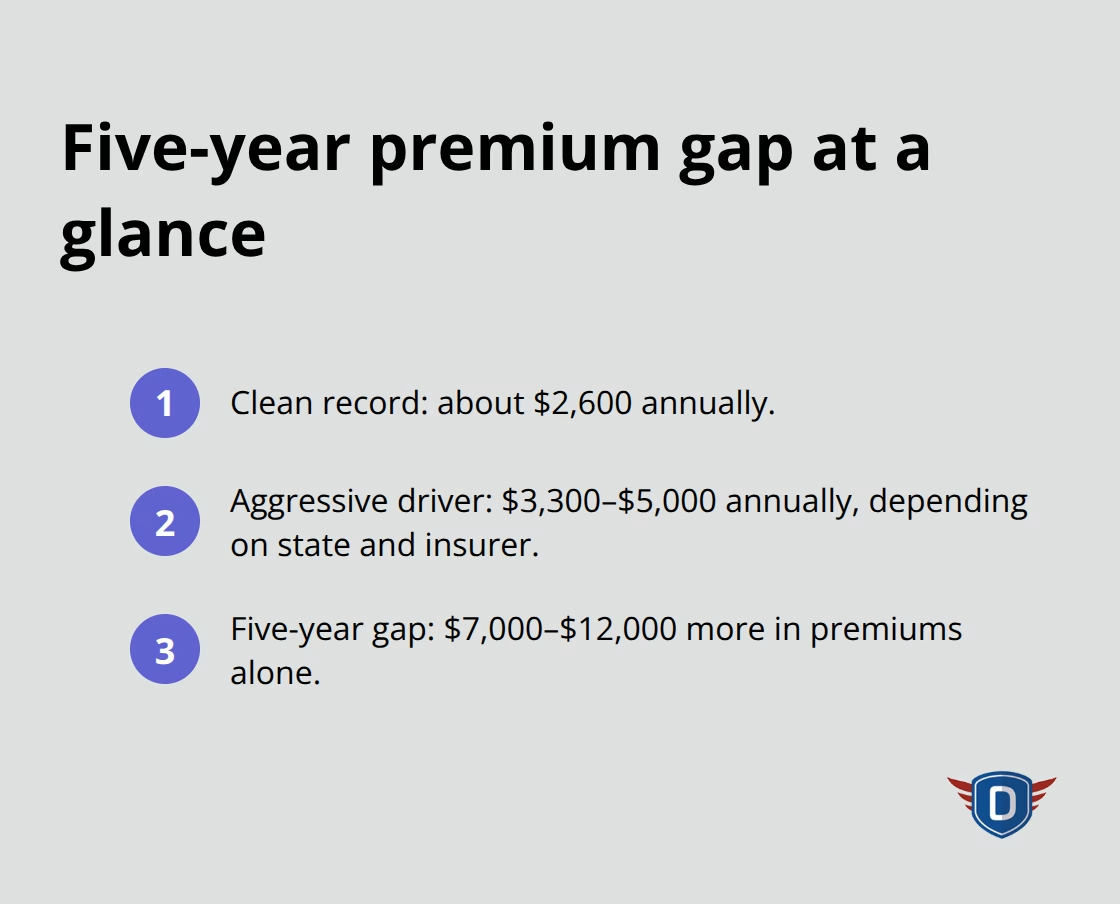

The gap between safe and aggressive drivers widens dramatically over a five-year period. A driver with a clean record might pay $2,600 annually, while an aggressive driver with a speeding ticket, a minor accident, and harsh braking patterns recorded through telematics could pay $3,300 to $5,000 depending on their state and insurer. Over five years, that’s a difference of $7,000 to $12,000 in premiums alone, and this calculation doesn’t include court costs, attorney fees, or the deductibles you’ll pay out of pocket.

How Technology Accelerates Change

Some insurers now co-fund safety technology and defensive driving programs, which means investing in better habits immediately reduces your rates rather than waiting years for violations to age off your record. The financial incentive to change your behavior is real and measurable, not theoretical. Telematics data can directly influence your next renewal quote, giving you immediate feedback on whether your driving changes are actually saving you money. This shift from punishing past mistakes to rewarding current safe behavior means that aggressive drivers who genuinely change their habits can see premium reductions within months rather than years.

Final Thoughts

Your aggressive driving consequences don’t have to define your insurance future. Telematics data shows that insurers reward behavioral change within weeks and months, not years, which means your next three months of driving can directly impact your next renewal quote. When you commit to safer habits, you create immediate financial incentive that transforms how you approach every trip.

Defensive driving techniques, proper following distances, and stress management skills require structured learning to stick. We at DriverEducators.com offer comprehensive programs designed to help you break aggressive patterns and adopt safer habits that reduce your insurance risk. Many insurers offer discounts when you complete a recognized driver improvement course, and these savings offset the course cost within months.

The financial reward for changing your behavior is substantial, and the safety benefit is immeasurable. Start with a driver improvement program that addresses your specific driving challenges, then monitor your telematics data to track your progress. Your next decision behind the wheel matters more than you realize.