Florida drivers overpay for car insurance every single day. The average Florida driver could save hundreds annually by understanding which car insurance discounts in Florida actually matter and which ones are marketing fluff.

At DriverEducators.com, we’ve seen firsthand how many drivers leave money on the table by not knowing where to look. This guide shows you exactly which discounts work, how to stack them, and what mistakes drain your savings fastest.

Which Discounts Actually Stack in Florida

Bundle Your Policies for Maximum Savings

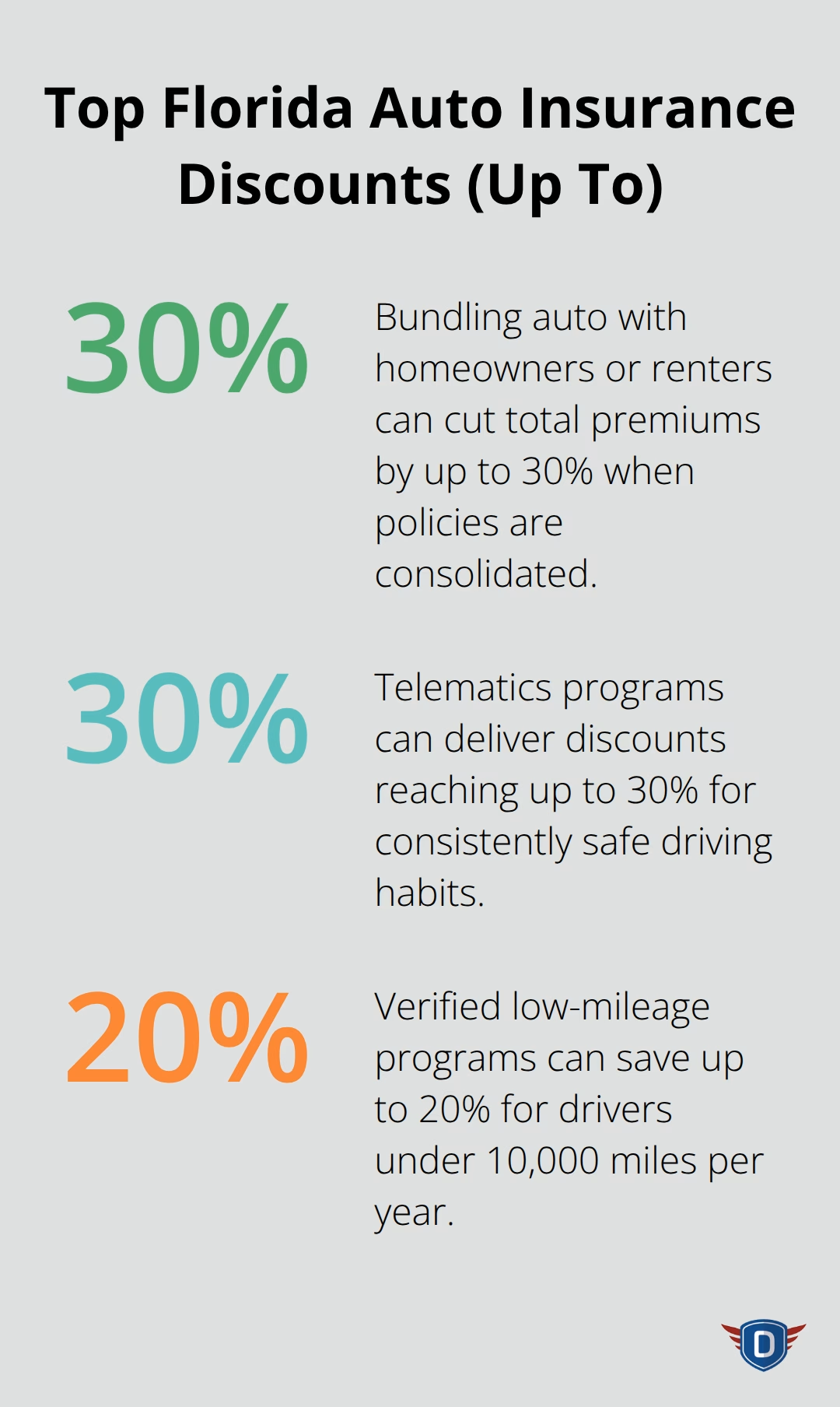

Bundling your auto policy with homeowners or renters insurance cuts your total premiums by up to 30%. This isn’t theoretical-insurers reward customer loyalty and reduce administrative costs when you consolidate coverage.

If you’re paying separate premiums for home and auto, you’re likely overpaying. When you consolidate, verify the bundled quote against separate quotes from competitors, because occasionally two separate policies beat a bundle. The math matters more than the marketing pitch. Florida drivers bundling auto with homeowners insurance typically see savings of $1,000 to $3,000 annually depending on coverage levels and the insurer. State Farm offers multi-line discounts for customers holding multiple policies, and Progressive bundles aggressively in Florida as well.

Safe Driving Pays Real Money

A clean driving record directly lowers your premium, and defensive driving courses amplify that benefit. Consumer Reports found that taking a defensive driving course saves approximately $233 annually on average. In Florida, drivers aged 55 and older who complete a Motor Vehicle Accident Prevention Course approved by the Florida Department of Highway Safety and Motor Vehicles can claim this discount by presenting the certificate to their insurer. Younger drivers benefit too-those under 25 who complete State Farm’s Steer Clear Safe Driver Program qualify for measurable savings. Enroll in a course before your renewal date hits, then present the certificate when shopping for quotes. You’ll see the discount reflected immediately in your rate calculations.

Academic Records Open Doors for Student Discounts

Good student discounts apply when drivers maintain a GPA of 3.0 or higher, typically saving 15–25% on premiums depending on the insurer. This discount targets drivers aged 16–25 still listed as students at accredited institutions. You need official documentation from your school showing your GPA to claim this benefit. When your student ages out of school or the GPA drops, the discount disappears at renewal, so track your eligibility closely. Many Florida families miss this discount entirely because they don’t realize it exists or forget to mention it when getting quotes. If you have a teen driver or young adult on your policy, pull their current transcript and provide it to your insurer-the savings compound across multiple years.

Telematics Programs Reward Safe Habits

Telematics programs track your driving behavior (speed, acceleration, braking, mileage) and reward safe habits with discounts. State Farm’s Drive Safe & Save program offers initial discounts plus potential additional savings for safe driving, with discounts reaching up to 30% or more in some cases. Progressive delivers similar programs across Florida. These programs require enrollment and ongoing participation in data collection, but the payoff justifies the effort for drivers who maintain consistent safe habits. Verify what data the program collects, how your information is used, and whether the insurer sells your data before enrolling. The discount potential makes telematics worth serious consideration, especially if you drive predictably and avoid aggressive maneuvers.

Stack Multiple Discounts for Bigger Savings

You can combine multiple discounts (bundling plus safe driver plus telematics, for example) to maximize your total savings, subject to eligibility and state rules. Florida’s rate environment has shifted dramatically-the state’s top five auto insurers averaged a 6.5% rate decrease in 2025, continuing relief after significant increases in prior years. Progressive alone is delivering nearly $1 billion in auto policyholder credits in Florida, with about 2.7 million Florida auto policyholders expected to receive credits by December 31, 2025. These credits stem from Florida auto insurance reforms that lowered loss costs and improved reserve development. When you shop for quotes, ask each insurer whether you qualify for credits or refunds tied to these reforms. The combination of stacked discounts and reform-driven credits creates a genuine opportunity to lower your costs without sacrificing essential protections-which makes the next step of comparing quotes across multiple insurers absolutely worth your time.

How to Actually Save Money on Your Car Insurance

Time Your Defensive Driving Course for Maximum Impact

Defensive driving courses deliver measurable savings, but only if you time them correctly and use them strategically. An approved course costs between $25 and $50 depending on the provider, yet saves roughly $233 annually according to Consumer Reports. For drivers aged 55 and older, completing an approved Mature Driver Discount course unlocks this discount immediately at renewal. Younger drivers under 25 qualify through State Farm’s Steer Clear Safe Driver Program.

Most drivers make a critical mistake by taking a course after their renewal date passes. Enroll before your policy renews, complete the course, and obtain your certificate. Present it directly to your insurer when requesting quotes. This timing ensures the discount applies to your next rate calculation rather than waiting another full year.

Shop Around and Capture Hidden Savings

Shopping around destroys the myth that your current insurer offers the best rate. Consumer Reports found that drivers who switched insurers in the past five years saved a median $461 annually, and this savings compounds over time. Florida’s rate environment shifted dramatically in 2025 when the state’s top five auto insurers averaged a 6.5% rate decrease, yet many drivers never captured these savings because they never requested fresh quotes.

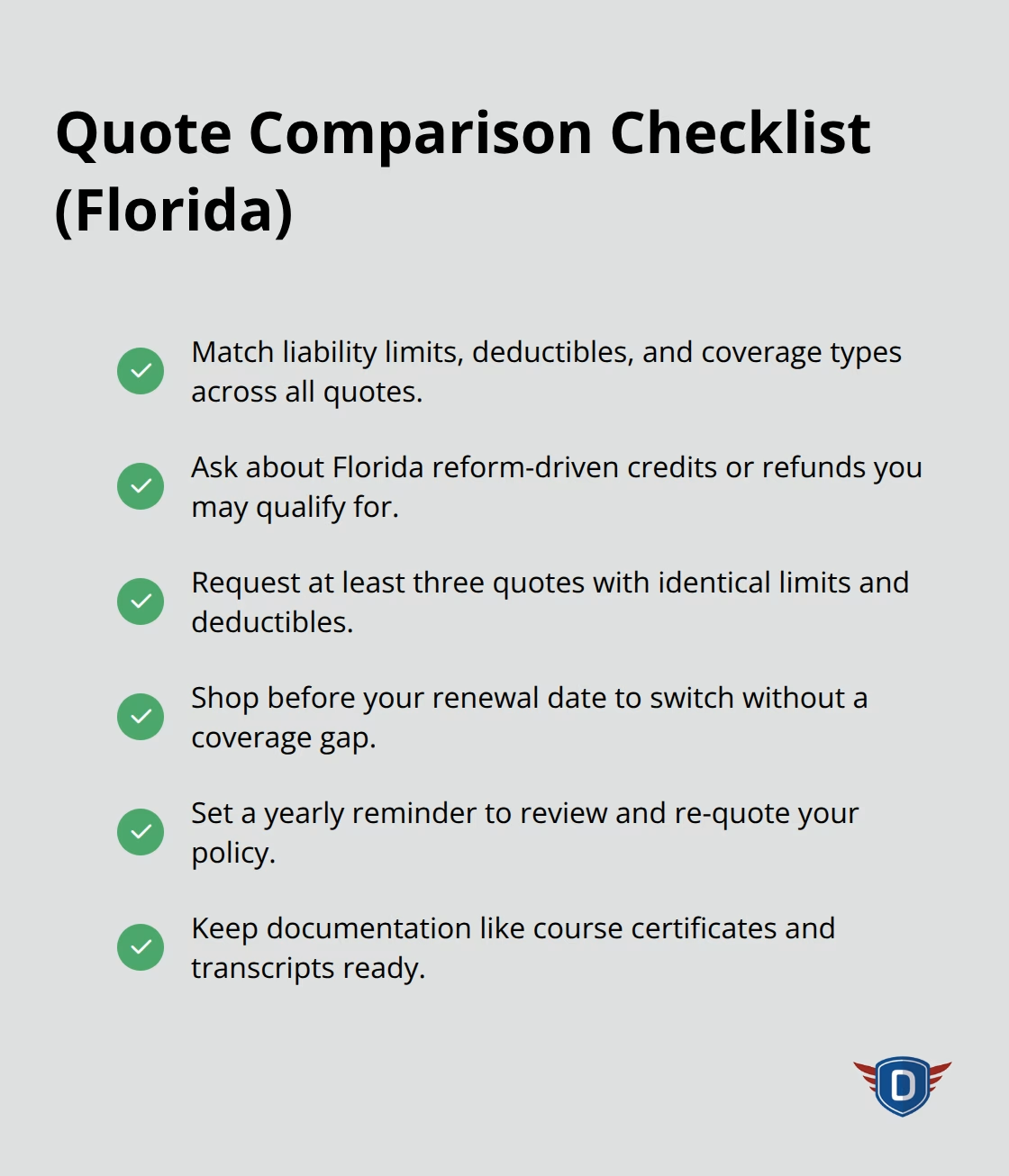

Progressive is delivering nearly $1 billion in auto policyholder credits in Florida to about 2.7 million policyholders by the end of 2025. These credits stem directly from insurance reforms. Your current insurer may or may not pass these savings to you automatically. Contact at least three insurers with identical coverage limits and deductibles to compare quotes and capture competitive pricing.

Verify Coverage Details When Comparing Quotes

When comparing quotes, verify that liability limits, collision deductibles, and comprehensive coverage match exactly across all quotes. Ask each insurer specifically whether you qualify for reform-driven credits or refunds available in Florida. Many drivers accept their renewal notice without questioning whether a competitor offers better rates, which costs them thousands over a decade.

Set a calendar reminder to shop quotes annually at minimum, and always do this before your renewal date so you have time to switch if a competitor offers substantially lower premiums. The savings opportunity (potentially hundreds of dollars per year) justifies the 30 minutes required to gather three competitive quotes. Your next step involves understanding which coverage mistakes drain your savings fastest, even after you’ve locked in a competitive rate.

Where Your Coverage Choices Cost You the Most

Liability Limits: The Most Expensive Mistake

Most Florida drivers choose liability limits based on state minimums rather than actual protection needs. Florida requires only $10,000 in Property Damage Liability and $10,000 in Personal Injury Protection, which sounds adequate until you cause an accident that injures multiple people or damages an expensive vehicle. A single serious crash generates medical bills exceeding $100,000, and if you’re found liable, your personal assets become vulnerable. Consumer Reports recommends carrying at least $100,000 in bodily injury liability per person and $300,000 per occurrence, which costs roughly $50–$100 more annually than state minimums but protects your financial future. Many insurers now offer umbrella policies starting around $250–$300 per year for $1 million in additional coverage, which fills gaps that standard auto policies leave exposed. The real money drain happens when drivers carry inadequate liability limits while thinking they’re saving money-one accident wipes out years of premium savings.

Collision and Comprehensive Coverage: When to Drop, When to Keep

Resist the urge to drop collision or comprehensive coverage just because your vehicle is older. If your car’s value has dropped significantly, dropping collision saves roughly $1,165 annually according to Consumer Reports, but this only makes sense if you can afford to replace the vehicle out of pocket. Your insurer depends on accurate information to calculate your rate correctly, yet most drivers never report changes in how they use their vehicle or who drives it.

Mileage Changes and Household Updates

If you shifted to working from home and now drive 8,000 miles annually instead of 15,000, your risk profile dropped significantly, but your premium won’t reflect this unless you tell your insurer. Drivers under 10,000 miles per year can save up to 20% through verified mileage programs, but you must actively enroll. Similarly, if a young driver moves off your policy or a household member stops commuting, your rate should decrease.

Annual Policy Reviews Capture Hidden Credits

Annual policy reviews catch these opportunities before renewal, when you’re already shopping quotes anyway. Set a calendar reminder every January to contact your insurer and confirm your coverage limits, deductibles, and household driver information match your current situation. This 15-minute conversation often reveals credits you’ve already qualified for but never claimed, particularly given Florida’s ongoing insurance reforms that generated nearly $1 billion in policyholder credits from Progressive alone in 2025. Drivers who ignore annual reviews accept whatever rate their insurer sends at renewal, which means they never capture savings from market improvements or their own changing circumstances.

Final Thoughts

Florida drivers who implement these strategies save hundreds annually while maintaining the coverage that actually protects them. A driver who bundles policies, qualifies for a safe driver discount, and enrolls in a telematics program can reduce premiums by $1,000 or more annually compared to someone accepting their renewal notice without question. Florida’s 2025 rate environment delivered a 6.5% average decrease among the state’s top five insurers, yet many drivers never captured these savings because they never requested fresh quotes.

The long-term benefit extends beyond lower premiums. Drivers who maintain adequate liability coverage, avoid coverage gaps, and stay informed about available car insurance discounts in Florida protect their financial future while keeping costs reasonable. One serious accident exposes drivers with inadequate liability limits to devastating personal liability, which erases years of premium savings instantly.

We at DriverEducators.com understand that safe driving habits directly influence your insurance costs. Our Florida-approved traffic school courses help drivers reduce points, meet court requirements, and qualify for discounts on car insurance in Florida, and you can explore our programs to see how our certified instructors support both your safety and your savings.